SUSTAINABILITY RELATED DISCLOSURES AT WHITE FUND ENTITY LEVEL

White Fund is a Belgian venture capitalist fund specifically dedicated to the medtech sector. White Fund positions itself as a high value-added investment fund. In addition to its finance mission, White Fund aims to support companies in the key stages of their development. Its multi-disciplinary team and extensive network, with experience of both medtech expertise and the world of investment, are key assets for portfolio companies.

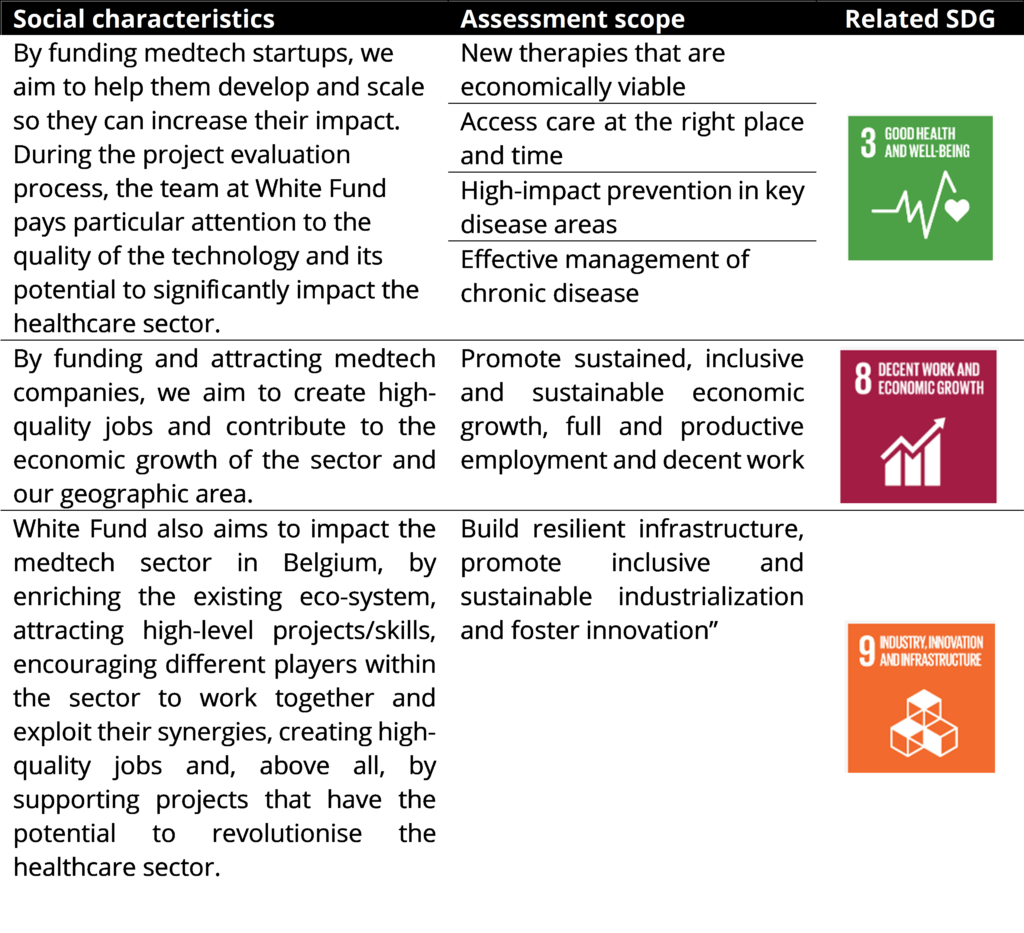

White Fund also aims to impact the medtech sector in Belgium, by enriching the existing eco-system, attracting high-level projects/skills, encouraging different players within the sector to work together and exploit their synergies, creating high-quality jobs and, above all, by supporting projects that have the potential to revolutionize the healthcare sector.

Below we share our sustainability related disclosures on entity level, and more specifically for the White Fund. From product perspective, in conformity with the requirements of Regulation (EU) 2019/2088 on sustainability-related disclosures in the financial sector (‘SFDR’).

Integration of sustainability risk in the investment policies

The Fund Manager considers sustainability risks as part of its investment decision-making process. Sustainability risks are environmental, social or governance events or conditions, the occurrence of which could have an actual or potential material adverse effect on the value of the investment.

The Fund Manager generally remains free in its decision to refrain from investing or to invest despite sustainability risks in which case the Fund Manager can also apply measures to reduce or mitigate any sustainability risks. The Fund Manager will apply the principle of proportionality in dealing with sustainability risks taking due account of the size and nature of the investment as well as its transactional context and the respective

margins for action. Risk analysis will be part of the due diligence process in the pre investment phase and will be formally repeated on an annual basis during the investment phase.

Principal adverse impact of investment decisions on sustainability factors

Currently White Fund does not consider principal adverse impacts of investment decisions on sustainability factors (i.e. environmental, social and employee matters, respect for human rights, anti‐corruption and anti‐bribery matters) in accordance with Article 4 of the SFDR (Regulation (EU) 2019/2088 of the European Parliament and of the Council of 27 November 2019 on sustainability-related disclosures in the financial services sector).

PAI data is often not readily available and is difficult to collect in early-stage companies. Therefore, the Fund Manager is not in a position to positively assume it will in all cases be able to always obtain sufficient information from portfolio companies to satisfy the disclosure obligations of Article 4 of the SFDR as further detailed in the Regulatory Technical Standards. The Fund Manager will review its policy on the integration of PAI’S when it will be in a position to provide such monitoring.

Integration of sustainability risk in the remuneration policy

As a sub-threshold manager of alternative investment funds, White Fund does not have an obligation to have a formal remuneration policy in accordance with article 40 and following of the Belgian law of 19 April 2014 on alternative entities for collective investments and their managers. As such, managing sustainability risk with its effects on fund revenues is not part of the remuneration criteria of the staff of White Fund.

SUSTAINABILITY-RELATED DISCLOSURES AT PRODUCT LEVEL

Summary

White Fund is a financial product that promotes environmental and/or social characteristics, but does not have as its objective sustainable investment and does not invest in sustainable investments. No reference benchmark has been designated for the purpose of attaining the environmental and/or social characteristics promoted by the Fund.

White Fund targets promising MedTech projects and is interested in companies that are actively developing medical devices, diagnostic and digital technologies at pre- commercialization phase.

The Fund’s mission is to:

- Bring cutting-edge innovation into real health care solutions;

- Improve the quality of life of patients and reduce medical costs;

- Enrich the Belgian medtech ecosystem by supporting the most promising companies.

The fund will integrate ESG principles in its investment cycle, provide monitoring and foresee support for the portfolio companies where needed.

The daily Fund management is characterized by a hands-on approach with a strong team and complementary Fund manager team that has the capacity to sharply analyze a wide variety of investment opportunities in short deadlines. In addition, the team can rely on a strong network of partners and co-investors who add investor focus, in depth research expertise and close-to-market medical care insights.

No sustainable investment objective

The Fund is considered an Article 8-type product under the SFDR, meaning that the fund promotes, amongst other characteristics, environmental or social characteristics, but does not have sustainable investments as its objective.

Environmental or social characteristics of the financial product

The Fund focuses on medical technologies, including medical devices, diagnostic and digital tools at pre-commercialization phase. Due to the nature of the investment focus, one may expect the main impact on social topics. Nevertheless, this does not exclude the possibility that a new technology could have a major positive impact on environmental impact, for example, when a technology can fully replace an old method or technology with a negative impact on environmental topics.

That being said, when assessing the impact of the scope of activities, the Fund manager team will use the following criteria:

Investment strategy

White Fund invests in all types of medical technologies, including prevention, diagnostic, monitoring and treatment solutions.

White Fund invests in early-stage projects entering commercialization. Depending on the project, early-stage can mean different things: as a minimum, projects must be able to demonstrate a soundproof of concept for their technology and/or an initial turnover that reflects the market appetite for the relevant product/service. For this reason, White Fund generally invests in the pre-market phases and the early commercialization phase, and/or in selected cases, in companies addressing the regulatory marking phase.

During the pre-investment phase, the Fund will assess the impact assessment scope topics, following a set of impact indicators, as foreseen in the general investment strategy of the fund. As part of the due diligence process, the team will also review risks and the effects of these related to environmental and social topics. Finally, a screening of the relevant governance topics are integral part of the process. Topics such as IT and data security, privacy and customer safety are topics which will receive extra attention.

During the investment cycle, the team will foresee an annual follow up of ESG topics and foresee the necessary monitoring and reporting processes. The Fund manager team will follow up on progress, based on the impact indicators and may define action points if necessary to mitigate risk exposure and negative impact. The White Fund team can rely on its own expertise on several sustainability related topics and will not hesitate to refer the portfolio companies to the broader network of experts within its ecosystem if more specialized support is needed.

Proportion of investments

In line with the ESG methodology, the Fund promotes environmental or social characteristics but does not commit to make only environmentally sustainable investments as defined in the Taxonomy Regulation; we do focus on sustainability and impact on a broader range. Consequently, we do not limit our investment scope only into companies that are in the ‘environmentally sustainable’ category.

The Fund does not intend to make sustainable investments as defined by the SFDR and therefore does not commit to investments in environmentally sustainable investments as defined in the Taxonomy Regulation (minimum percentage of investments in accordance with the Taxonomy Regulation: 0%). The underlying investments of that financial product do not take into account the EU criteria for environmentally sustainable economic activities.

Monitoring of environmental or social characteristics

The Fund Manager constantly monitors the environmental and social characteristics and performance of the Fund. For that purpose, our portfolio companies are required to report on ESG KPIs at least once per year.

The ESG reporting of each portfolio company is assessed by the Fund Manager team. The results and findings are examined with the Partner, who can bring ESG risks and opportunities to the attention of the Board of the respective company.

Methodologies

The Fund aims to implement an ESG evaluation tool designed specifically for the medtech sector. This tool allows us to assess the companies based on several KPI’s. When the company is funded, those KPI’s are monitored each year.

Data sources and processing

Portfolio companies report their financial performance and Impact KPIs on an annual basis. Each investment manager in the Fund is responsible for reviewing the data and following up on the progress towards achieving ESG-related targets. ESG and the financial performance of the portfolio are reported to our investors on a quarterly basis, or at least on an annual basis.

Further, the Fund manager team will rely on the knowledge and experience of the internal White Fund team and when necessary, the team can reach out to the broad network of experts to benchmark available data.

No formal external benchmarks or data sources will be used for monitoring and reporting.

The annual reports will be shared with the fund stakeholders. If the Fund manager team assumes that further action and monitoring is needed, or escalation is required they will take the necessary actions to address this issue in the existing governance bodies.

Limitations to methodologies and data

The information collected via the Funds Manager’s due diligence process and throughout the lifecycle is externally verified only if and to the extent misrepresentations are suspected. Reliability of data obtained from external sources cannot be guaranteed. As the Fund’s investment is made for several years, the Fund Manager considers it a priority to establish and maintain a trustful working relationship with the Fund’s portfolio companies in order to ensure compliance with the restrictions described in this section.

Due diligence done on underlying assets regarding ESG criteria

All investment decisions are based on commercial, financial, legal, and ESG due diligence, as well as estimated return and key risk components. During the due diligence process, all potential portfolio companies will be asked to complete a detailed ESG questionnaire to give us insights into the materiality of ESG risks, or share the necessary information needed if the requested information is already available.

Prior to each investment, ESG risks and opportunities are evaluated in a due diligence process. No further reviews will be conducted beyond such due diligence process unless the Fund Manager deems it appropriate. In such case it may be necessary to develop an action plan to mitigate possible risks or negative impacts. Such action plan is then formalized in the legal documents.

This is clearly formulated but not reflected accordingly:

- Knowing the investment strategy & focus , what are the main risks;

- What are main neg impacts;

- Whats are + impacts;

- How do companies perform? What actions did the fund take to improve/support the portfolio companies.

The post-investment follow-up and monitoring can be found in the topics ‘investment strategy’, ‘monitoring’, ‘methodologies’ and ‘data sources and processing’.

Engagement policies

Should the Fund Manager on behalf of the Fund determine any potential issues relating to environmental or social characteristics, the Fund Manager will engage in discussions with the portfolio company’s manager in order to resolve such issues, provided that such efforts will always remain at a level that the Fund Manager, in its sole discretion, considers to be proportionate in light of the size and strategic importance of the respective investment in the portfolio companies and that takes into account the respective negotiation positions and transactional context.

Information on any designated reference benchmarks used

The Fund does not use any reference benchmark.

Date: June 27th, 2023